Mexico’s Economic Outlook: Why Deeper U.S. Integration Still Shapes Nearshoring Decisions

Executive Introduction

As global trade uncertainty intensifies, Mexico finds itself navigating a complex but familiar position: highly exposed to U.S. economic cycles, yet structurally embedded in North American manufacturing in ways that are difficult to unwind.According to BBVA Research, the most likely medium-term scenario is not decoupling, but deeper industrial integration between Mexico and the United States, even under renewed tariff pressure.

For companies evaluating nearshoring in Mexico, the relevant question is no longer whether geopolitical volatility exists—it clearly does—but how resilient Mexico’s industrial platform remains under stress, and what this means for production, logistics, and site-selection decisions through 2026.

This article analyzes the latest Mexico outlook with a focus on U.S. integration, based on BBVA Research data, and translates macroeconomic signals into practical implications for manufacturing footprints and industrial real estate planning.

Global Trade: Tariffs Are Higher, but Reality Is More Nuanced

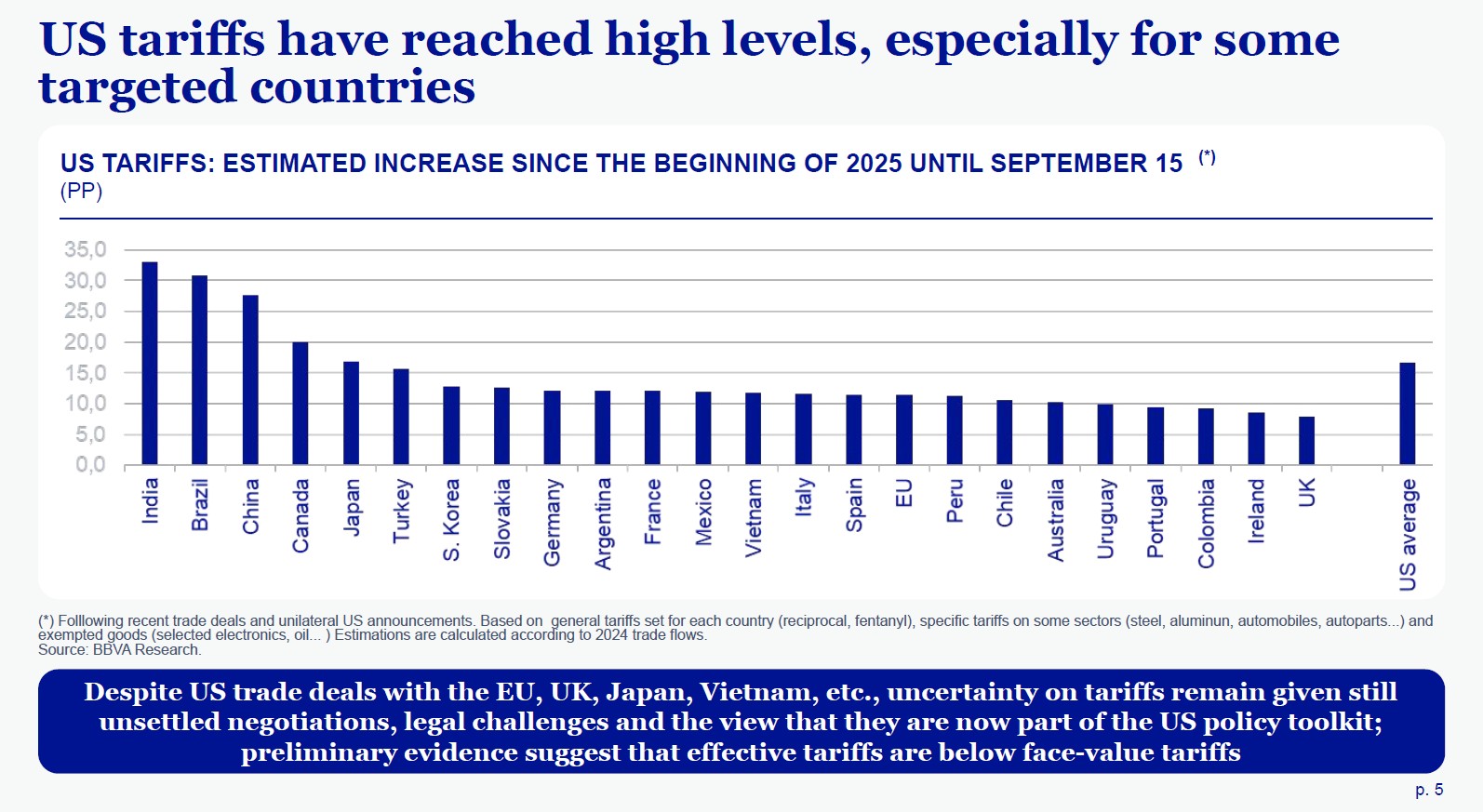

Global trade entered 2025 under renewed tariff escalation, particularly from the United States.BBVA Research documents that headline tariffs announced by the U.S. reached historically high levels, especially for targeted countries such as China, Brazil, and parts of Asia.

However, effective tariffs—the ones actually paid—remain significantly lower than face-value rates.

Figure 1 (after this section): U.S. Tariffs – Estimated Increase vs. Effective TariffsThis chart compares announced tariff levels with effective tariffs calculated from U.S. fiscal data. It shows that exemptions, trade deals, and product carve-outs materially reduce real tariff exposure.

Key takeaway:Tariffs are now a persistent policy tool, but their economic impact is filtered through exemptions, USMCA rules, and supply-chain realities. This distinction is critical when assessing Mexico’s competitive position.

Global Growth Is Slowing—But Not Collapsing

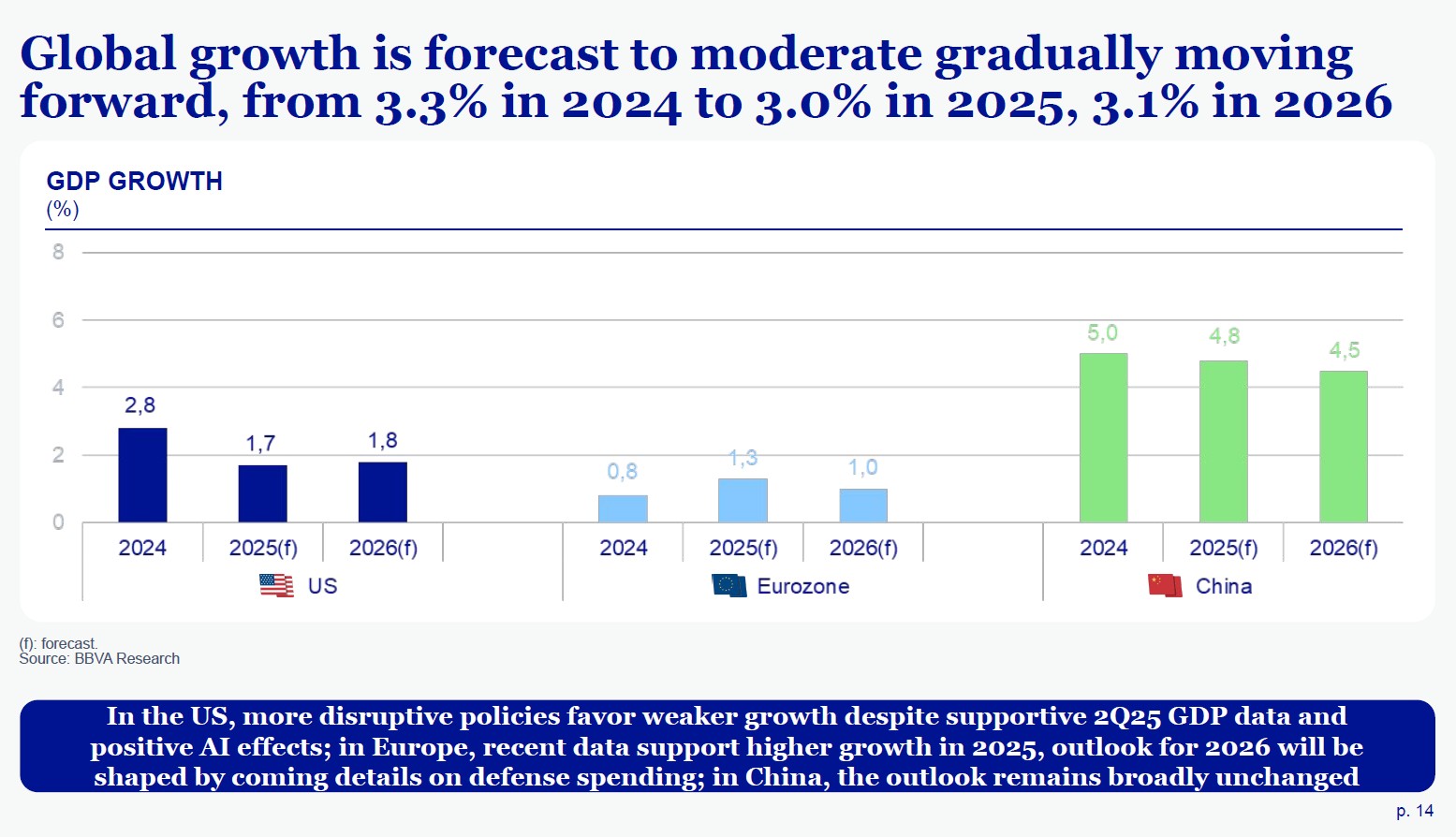

BBVA Research forecasts moderating global growth, not a recessionary collapse:

- Global GDP: ~3.0% in 2025 and ~3.1% in 2026

- U.S. growth softens under policy uncertainty

- Europe stabilizes modestly

- China remains constrained by structural deflation risks

Figure 2: Global GDP Growth Forecast (2024–2026)This bar chart shows gradual deceleration rather than abrupt contraction, reinforcing the view that global demand remains intact but cautious.

For Mexico, this matters because nearshoring depends more on relative competitiveness than absolute global growth rates.

Mexico’s Growth Has Slowed—Driven by Domestic Factors

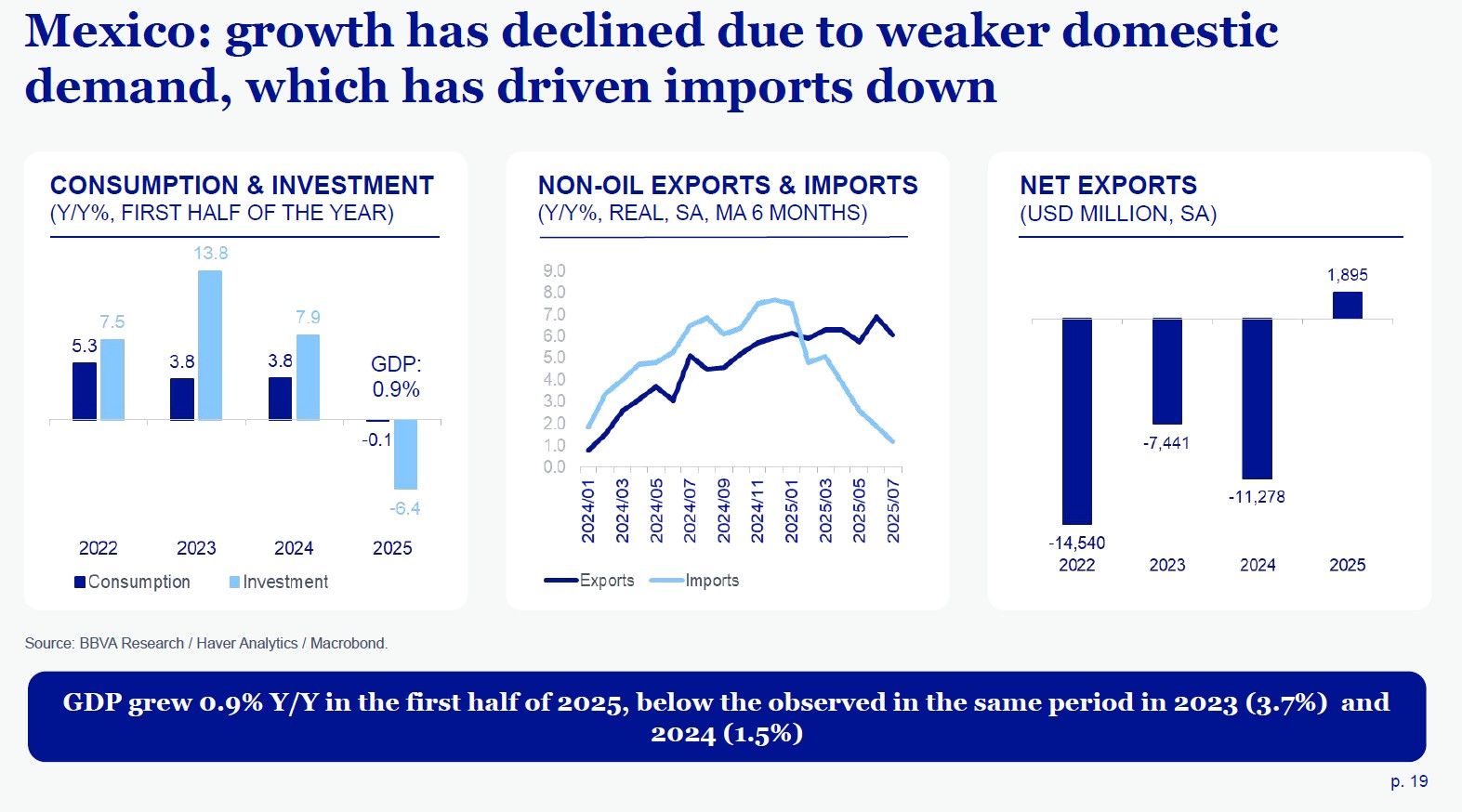

Mexico’s GDP growth reached 0.9% year-on-year in the first half of 2025, down from 1.5% in 2024 and well below 2023 levels.BBVA attributes this slowdown primarily to weaker domestic demand, not external collapse.

Figure 3: Mexico – Consumption, Investment, and Net ExportsThe chart illustrates declining investment and consumption, while net exports improve temporarily due to front-loaded shipments ahead of tariffs.

Interpretation:Mexico’s economy is adjusting internally (fiscal tightening, high interest rates, institutional changes), while external manufacturing links remain resilient.

Mexico–U.S. Manufacturing Integration Remains Structural

One of the clearest findings in the BBVA report is the depth of Mexico’s manufacturing integration with the U.S.:

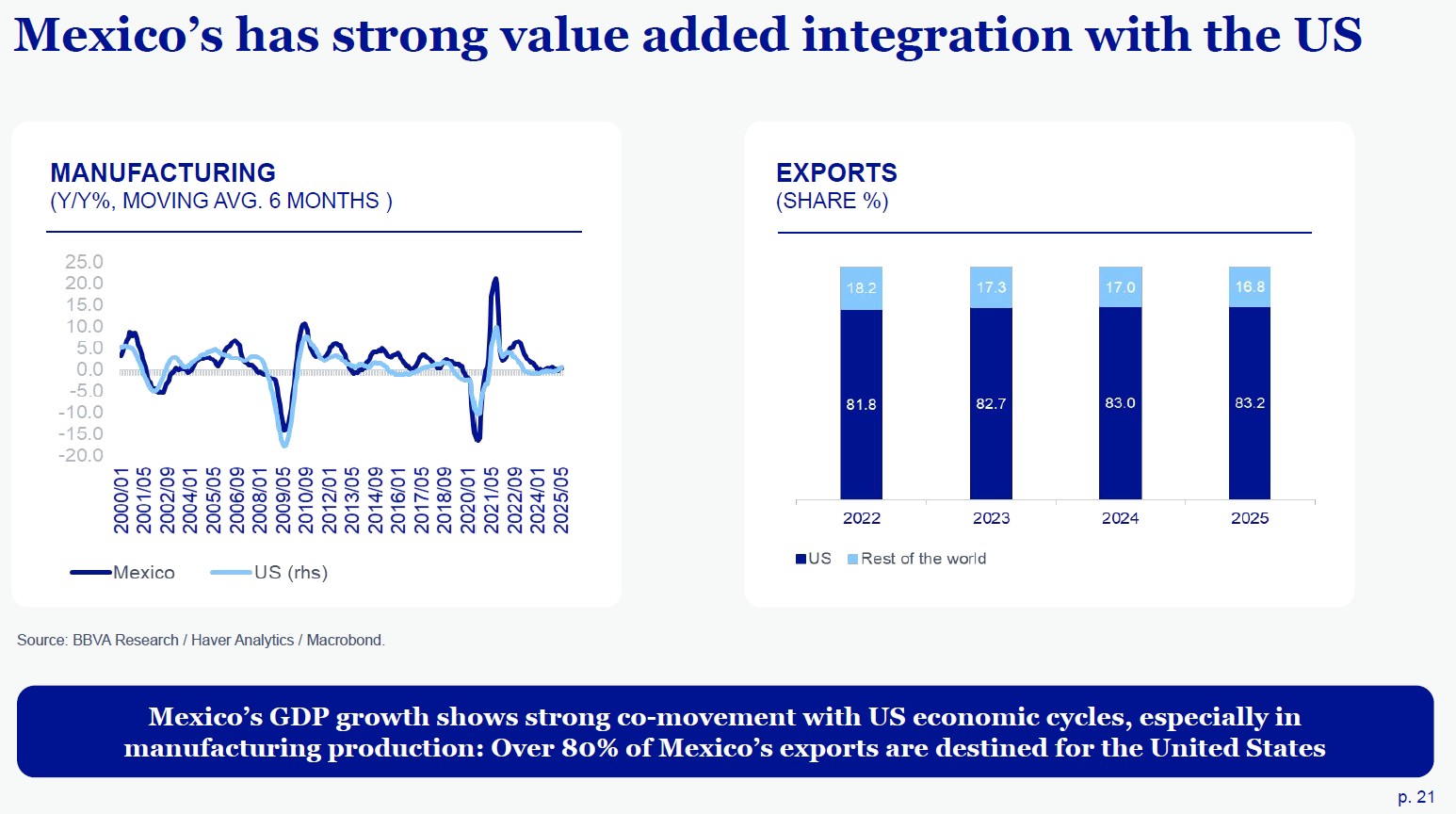

- Over 80% of Mexican exports are destined for the United States

- Manufacturing output in Mexico shows strong co-movement with U.S. industrial cycles

- On average, 22% of the value added in Mexican manufacturing exports comes from U.S. inputs

Figure 4: Manufacturing Co-movement and Export Share to the U.S.This visualization compares U.S. and Mexican manufacturing output trends and highlights export concentration.

What this means for nearshoring:Mexico is not a peripheral supplier—it is part of the same production system. Relocating production away from Mexico would imply rebuilding entire supplier ecosystems elsewhere.

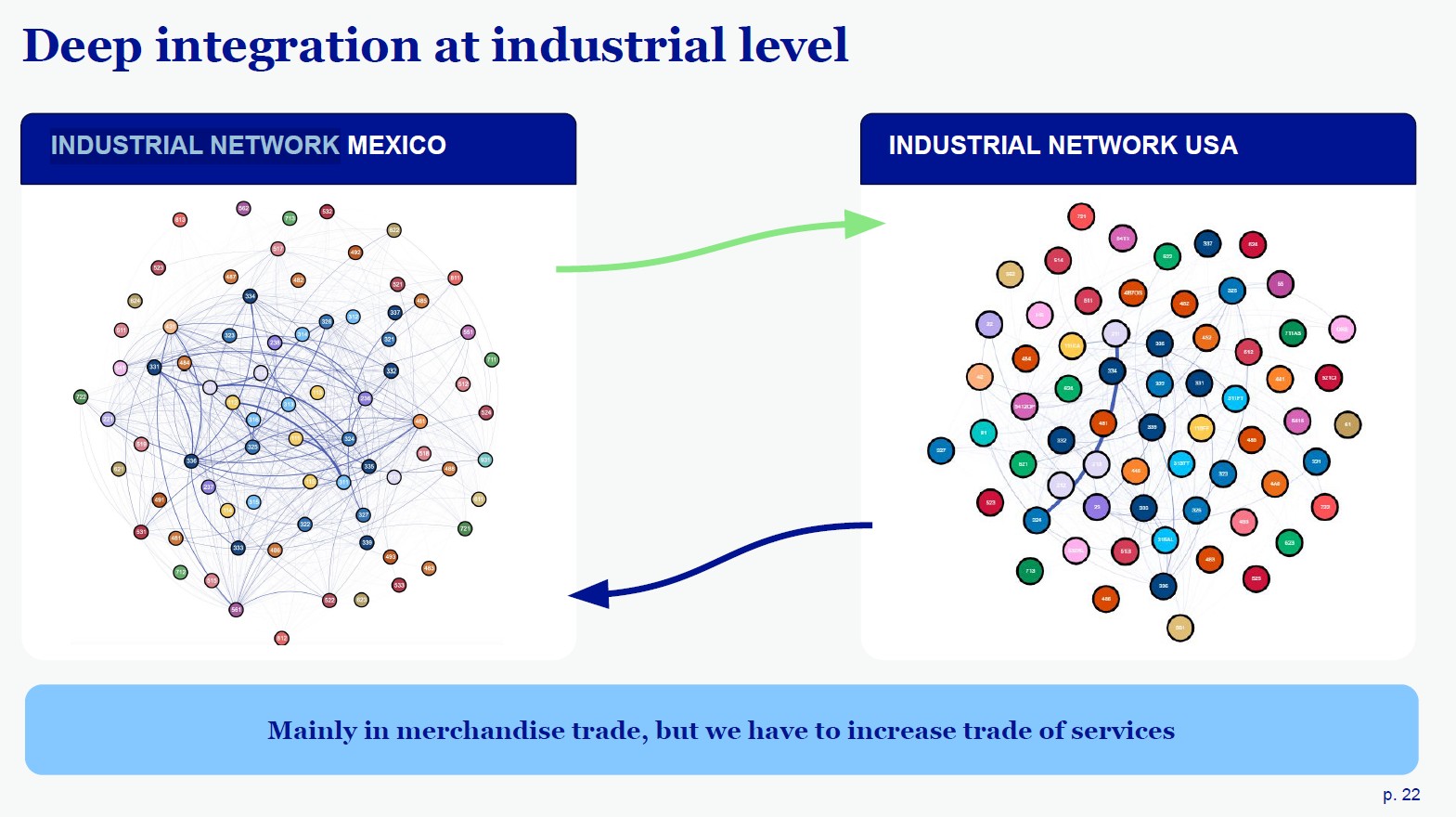

Industrial Networks: Why Geography Still Wins

BBVA Research illustrates industrial integration using network diagrams that map cross-border production linkages, particularly between Texas and Northern/Central Mexican industrial states.

Figure 5: Industrial Network – Mexico vs. United StatesThe diagram shows dense interconnections in machinery, transportation equipment, metals, electronics, and chemicals.

A second diagram highlights how Texas exports feed directly into Mexico’s transportation equipment and manufacturing networks, underscoring why logistics proximity matters.

Decision insight:Nearshoring is not just about labor cost—it is about network density, time-to-market, and supply-chain resilience, all of which favor Mexico’s industrial corridors.

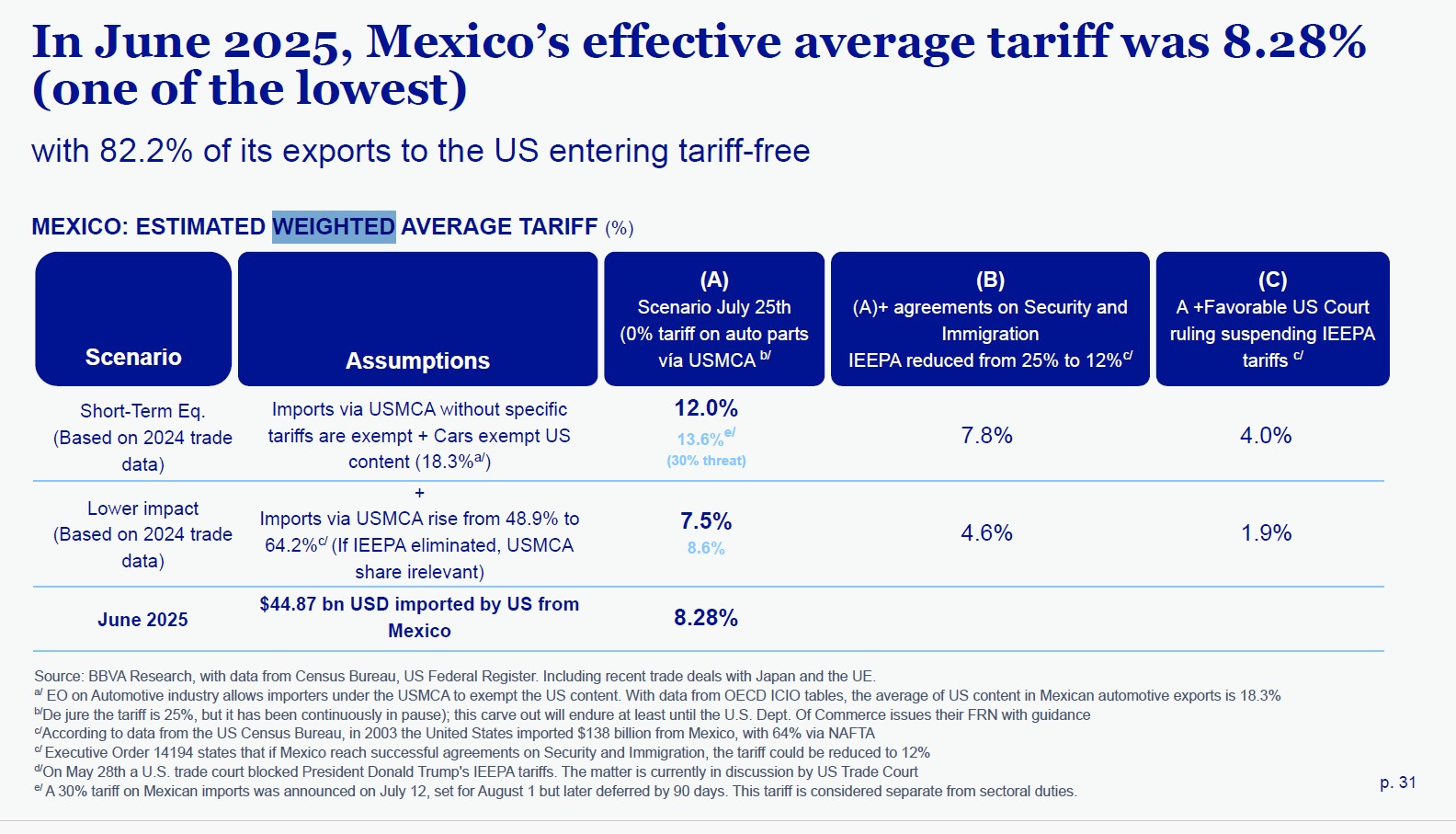

Tariffs and USMCA: Mexico Still Faces Lower Relative Protectionism

Despite political noise, Mexico continues to enjoy a more favorable tariff position than most U.S. trading partners:

In June 2025, Mexico’s effective average tariff was ~8.3%, among the lowest globally

82% of Mexican exports to the U.S. entered tariff-free

Even under adverse scenarios, Mexico’s tariff burden remains below that of Asia and parts of Europe

Figure 6: Weighted Average Tariffs – Global ComparisonA world map and line chart illustrate Mexico’s relatively low effective tariff exposure.

Key implication:Tariffs are a risk—but relative competitiveness matters more than absolute tariff levels.

Manufacturing Competitiveness: Beyond Low Costs

BBVA’s Revealed Comparative Advantage (RCA) analysis shows Mexico ranking Top 1 or Top 2 globally in multiple manufacturing segments, including:

- Transportation equipment

- Electrical equipment and components

- Machinery

- Fabricated metal products

Figure 7: Mexico’s Revealed Comparative Advantage by SectorThis table and index demonstrate that Mexico’s competitiveness is structural, not temporary.

Importantly, Mexico’s manufacturing wages remain significantly lower than China’s, while logistics and USMCA rules offset tariff differentials.

Plan México: Policy Support for Industrial Investment

The report also references Plan México, unveiled in late 2024, which expands fiscal incentives for industrial investment:

- Accelerated depreciation for new fixed assets

- Additional deductions for workforce training

- IMMEX 4.0 simplification for VAT and IEPS certification

- Target: +15% domestic content in key industries by 2030

While implementation risks remain, the framework signals policy alignment with nearshoring-driven industrial expansion.

Outlook: What This Means for Industrial Location Decisions

Based on the latest available data (2024–2025), BBVA Research concludes that:

- Mexico will likely face below-trend growth, but no inflationary crisis

- Deeper U.S. integration remains the most probable scenario

- Tariffs will persist, but Mexico retains a relative advantage

- Industrial investment decisions will be more selective, not reversed

For companies evaluating industrial real estate in Mexico, this points to a shift from speculative expansion to targeted site selection, focusing on:

- Existing industrial clusters

- Cross-border logistics efficiency

- Energy and infrastructure availability

- Skilled labor pools

FAQ – Questions Decision-Makers Ask

Is nearshoring in Mexico still viable under tariff uncertainty?Yes. Tariffs are a factor, but Mexico’s relative position within North America remains strong.

How dependent is Mexico on the U.S. market?Highly. Over 80% of exports go to the U.S., making integration structural rather than optional.

Are tariffs fully passed on to manufacturers?No. Effective tariffs are often much lower than announced rates due to exemptions and USMCA rules.

Does slower GDP growth reduce industrial opportunities?Not necessarily. Manufacturing integration and export demand remain resilient despite domestic slowdown.

Is Mexico competitive beyond labor costs?Yes. RCA data shows strong competitiveness in machinery, transport equipment, and electronics.