Strait of Hormuz Disruption: Why Nearshoring in Mexico Could Gain Momentum

Executive Summary

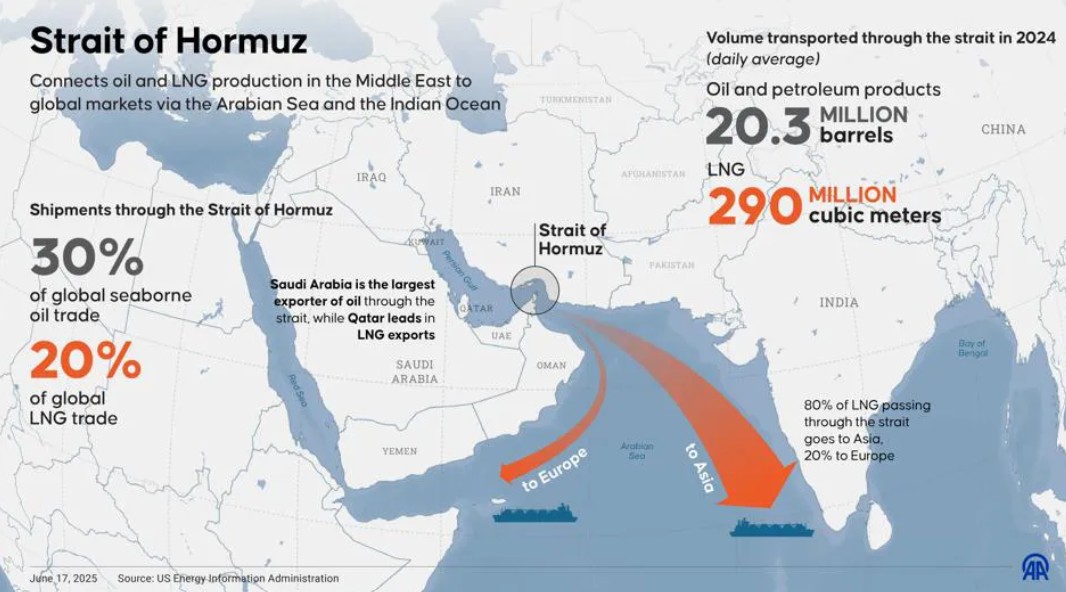

The Strait of Hormuz is one of the most critical energy chokepoints in the global economy. Roughly one-fifth of the world’s traded oil and LNG passes through this narrow waterway connecting the Persian Gulf to global markets.

Recent military escalation between the United States and Iran has sharply increased geopolitical risk in the region. Energy infrastructure has been targeted, shipping insurers have raised war-risk premiums, and tanker traffic through the strait has slowed significantly.

Energy markets reacted immediately. Within days:

- Brent crude oil rose roughly 10%

- European natural gas prices surged up to 40–60%

- global logistics companies began preparing for freight disruptions and capacity shortages

For companies supplying the North American market, these developments highlight a structural shift in supply chain strategy. As geopolitical risks affect energy costs and global logistics, nearshoring in Mexico becomes increasingly attractive as a resilience strategy.

Mexico offers proximity to the United States, integration into the North American energy system, and shorter logistics routes compared with Asian production hubs.

Why the Strait of Hormuz Matters for Global Supply Chains

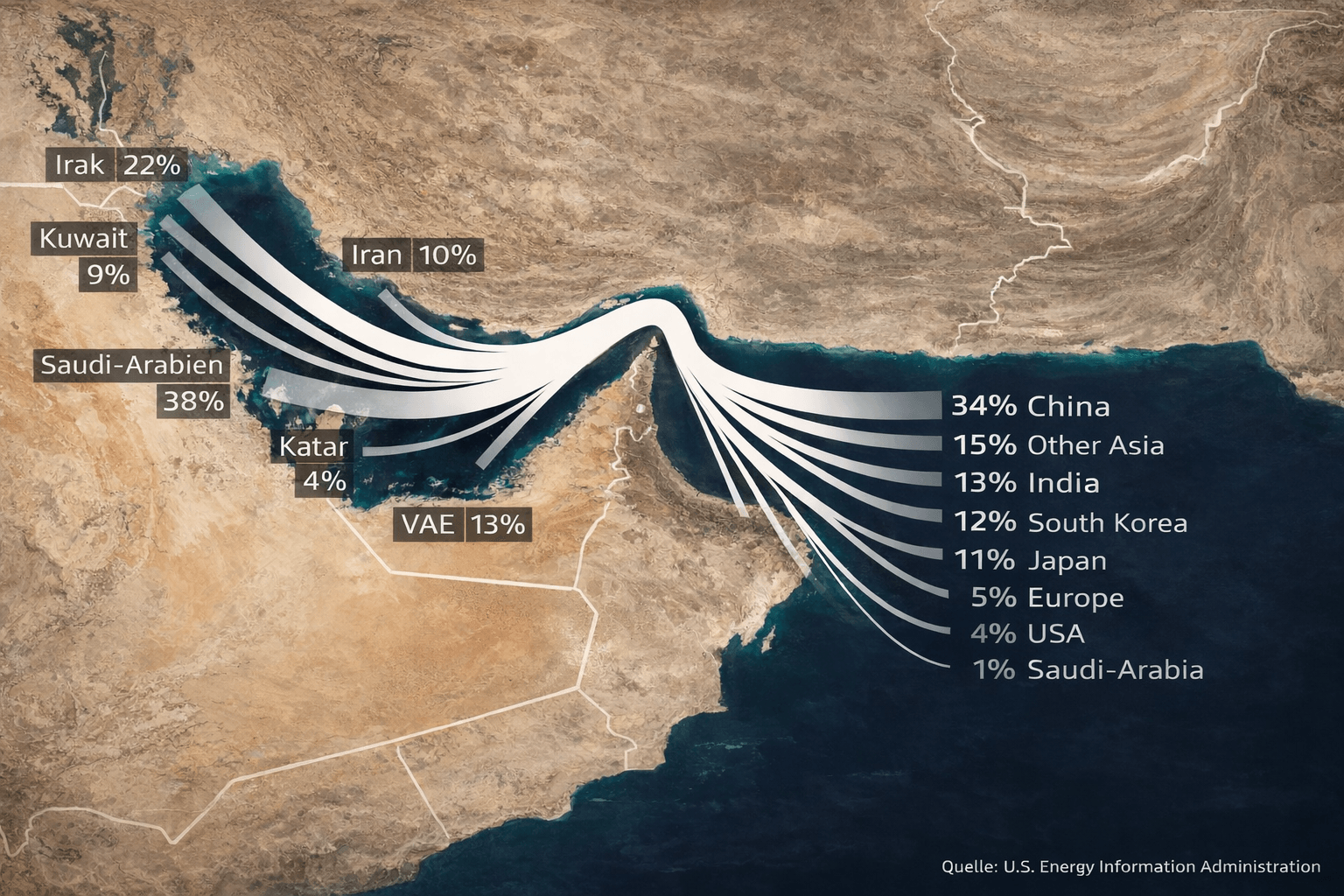

The Strait of Hormuz connects the Persian Gulf with the Arabian Sea and the Indian Ocean. Because of its geography, it functions as one of the most important transport corridors in the global energy system.

Approximately 20% of global oil and LNG trade moves through the strait every day. This includes exports from major energy producers such as:

- Saudi Arabia

- United Arab Emirates

- Iraq

- Kuwait

- Qatar

- Iran

These flows are particularly important for Asian economies, which depend heavily on imported energy resources.

Diagram: Global oil and LNG flows through the Strait of Hormuz showing exports from Gulf producers to major Asian markets such as China, India, Japan, and South Korea.

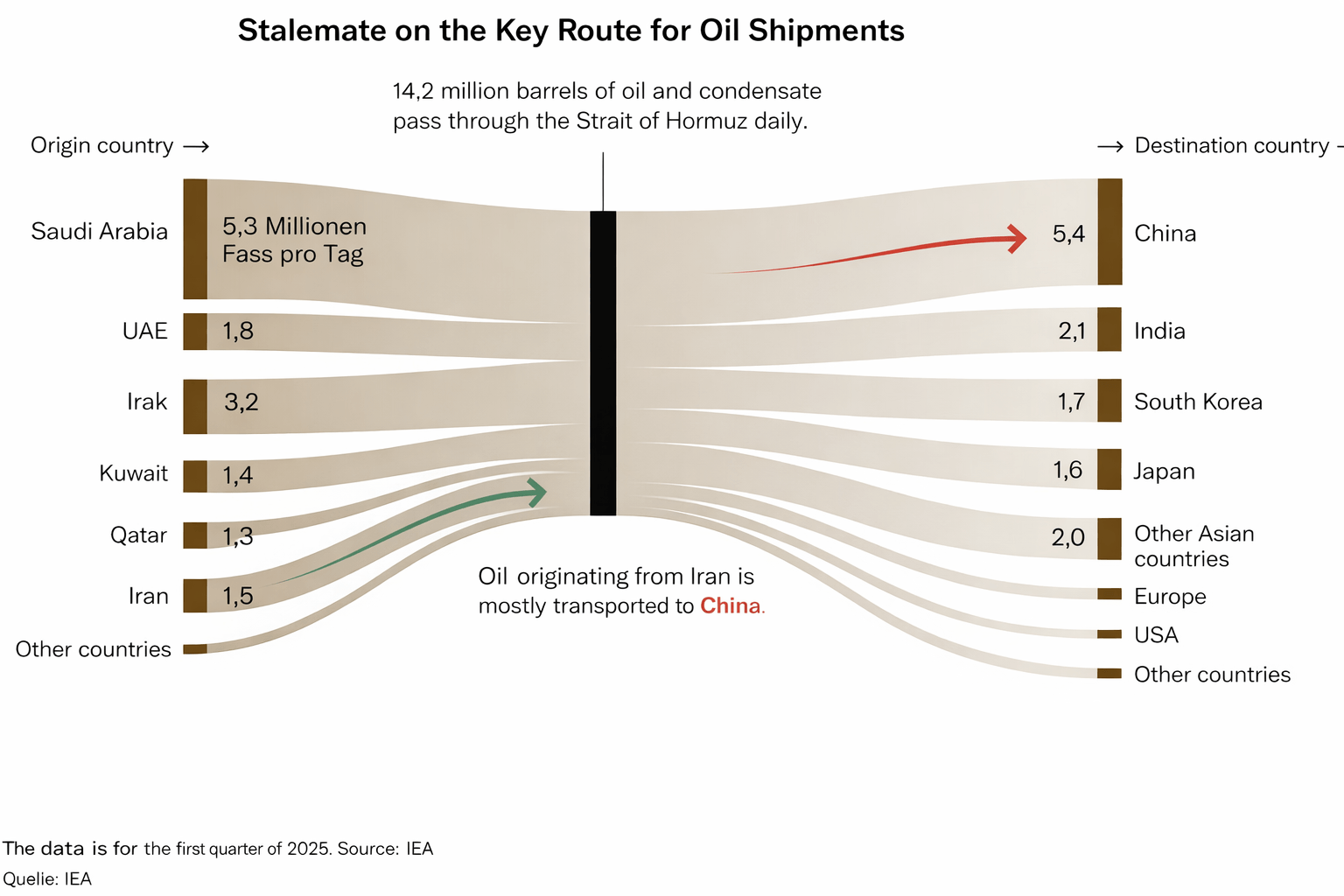

Daily shipments through the strait typically include more than 14 million barrels of crude oil and condensates.

Because alternative transport routes are limited, even small disruptions can have significant effects on global energy markets.

Only around one-third of the oil normally transported through the strait could theoretically be redirected through pipelines to other export terminals.

What Changed in Late February 2026

Tensions escalated sharply in late February 2026 after U.S. and allied military strikes targeted Iranian positions.

In response, several energy facilities across the region were attacked or temporarily shut down. These included:

- a major LNG export installation in Qatar

- the Ras Tanura oil refinery in Saudi Arabia

- energy terminals in the United Arab Emirates

These events quickly triggered concerns about energy supply disruptions and shipping safety in the Persian Gulf.

Even though the strait remains technically navigable, tanker traffic has declined significantly because insurers have raised war-risk premiums and shipping companies are avoiding the region.

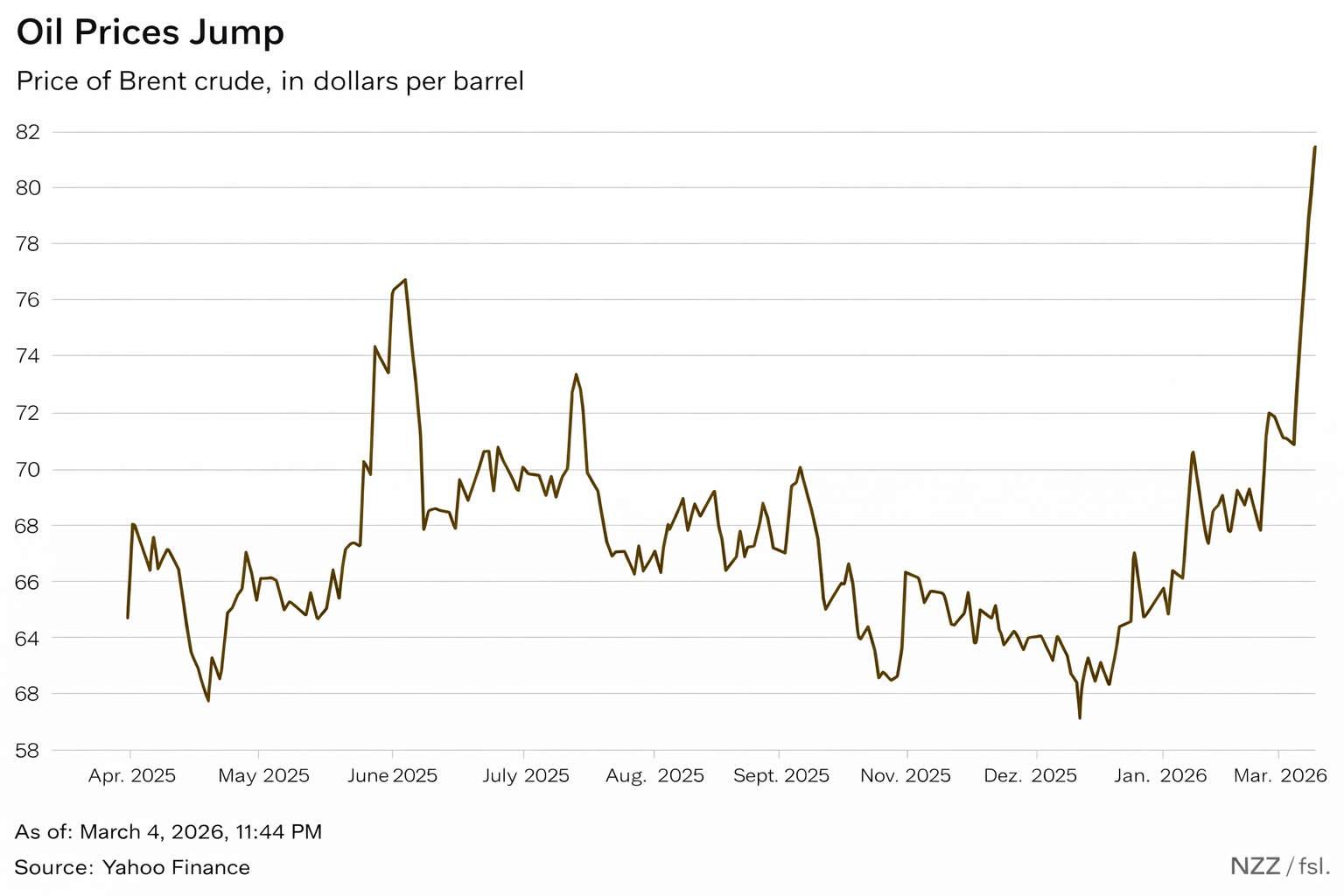

Energy Markets React: Oil and Gas Prices Surge

Energy markets responded immediately to the escalating geopolitical risks.

Diagram: Brent crude oil prices rising sharply to around $80 per barrel in March 2026 following escalating tensions near the Strait of Hormuz.

Within days of the conflict escalation, the price of Brent crude oil rose from roughly $73 to nearly $80 per barrel, representing an increase of about 10 percent.

Natural gas markets reacted even more dramatically.

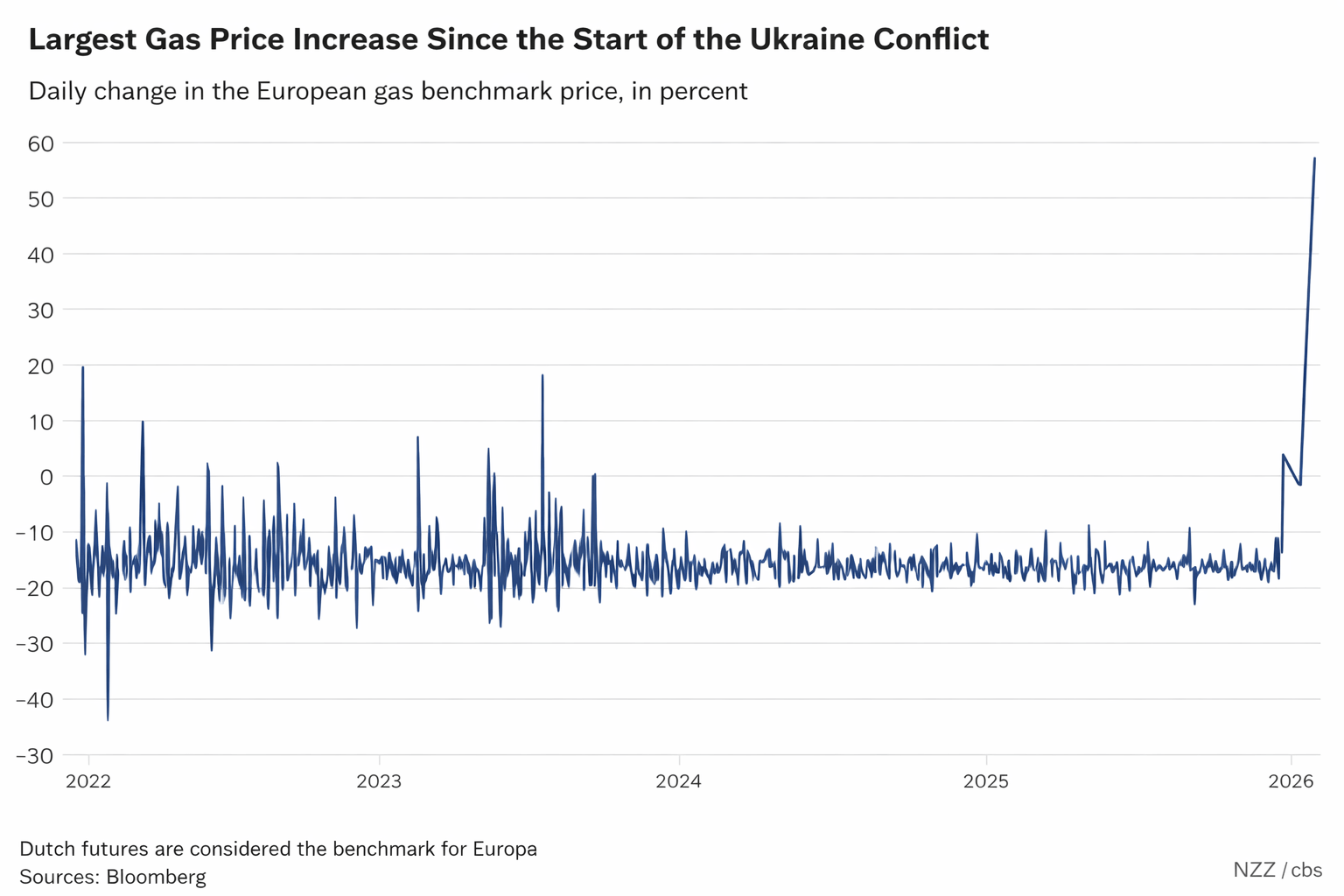

Diagram: European natural gas price volatility showing the largest spike since the Ukraine war amid Middle East energy disruptions.

European benchmark gas prices recorded the largest daily increases since the start of the Ukraine conflict in 2022, with some movements reaching 40–60 percent.

Gas markets are structurally more volatile than oil markets, and disruptions to LNG exports from the Gulf region can quickly tighten global supply.

At the same time, European gas storage levels remain relatively low, with reserves currently estimated at around 30 percent of capacity.

Logistics Impact: Air Cargo Capacity Disruptions

The conflict is not only affecting energy markets—it is also beginning to disrupt global logistics.

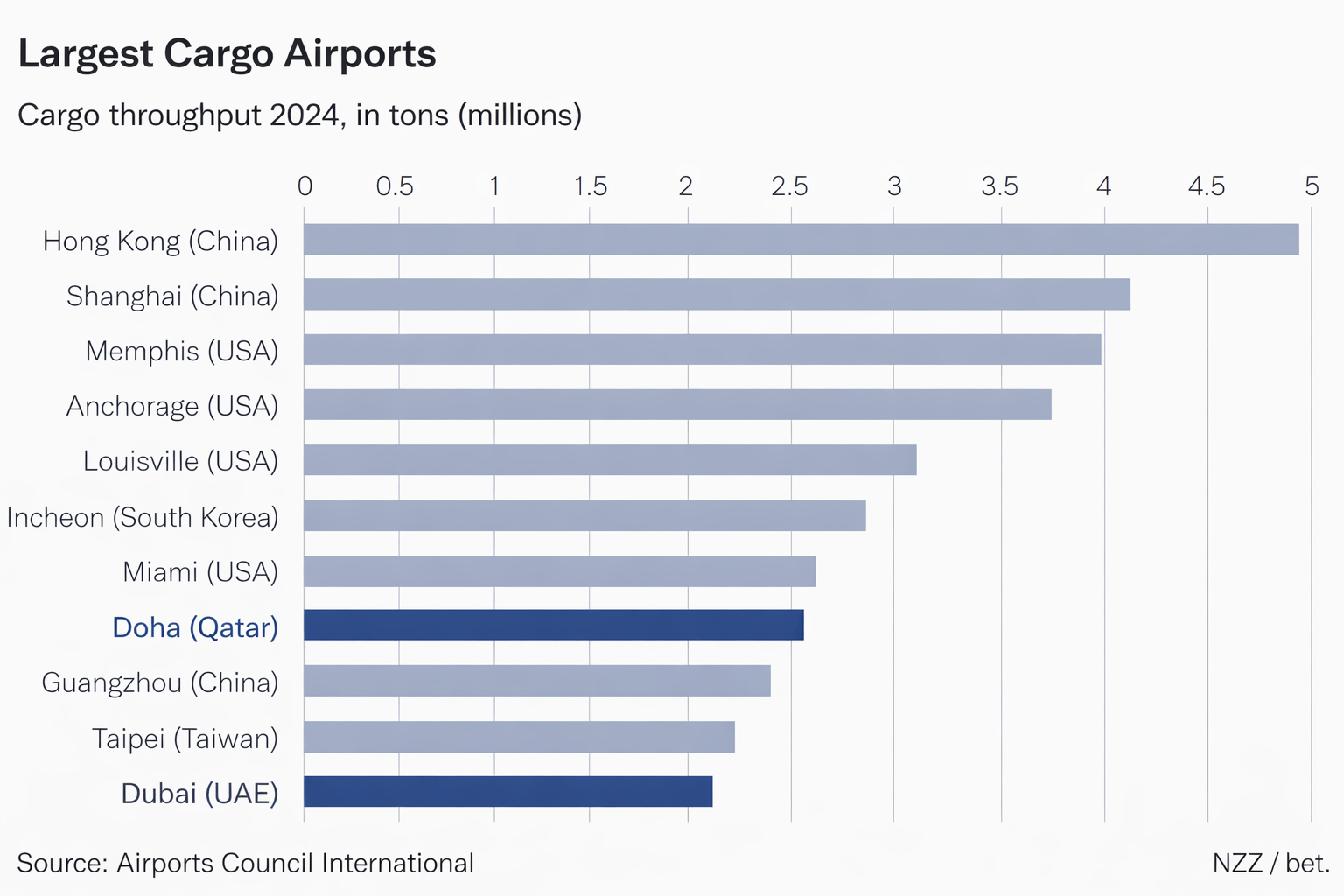

Several airports in the Gulf region temporarily suspended operations, grounding aircraft fleets that normally serve as major cargo hubs.

Industry estimates suggest that approximately 18 percent of global air cargo capacity may currently be unavailable due to grounded aircraft.

Diagram: Ranking of the world’s largest cargo airports including Hong Kong, Shanghai, Memphis, Anchorage, and Doha.

Cargo capacity reductions can quickly affect supply chains because freight is often transported in the belly space of passenger aircraft.

Logistics operators are already chartering additional cargo planes to maintain global transport flows.

However, these charter flights are expensive. A single cargo charter flight between Asia and Europe currently costs roughly $450,000, and prices could increase further if disruptions persist.

Global Shipping Routes and Container Trade

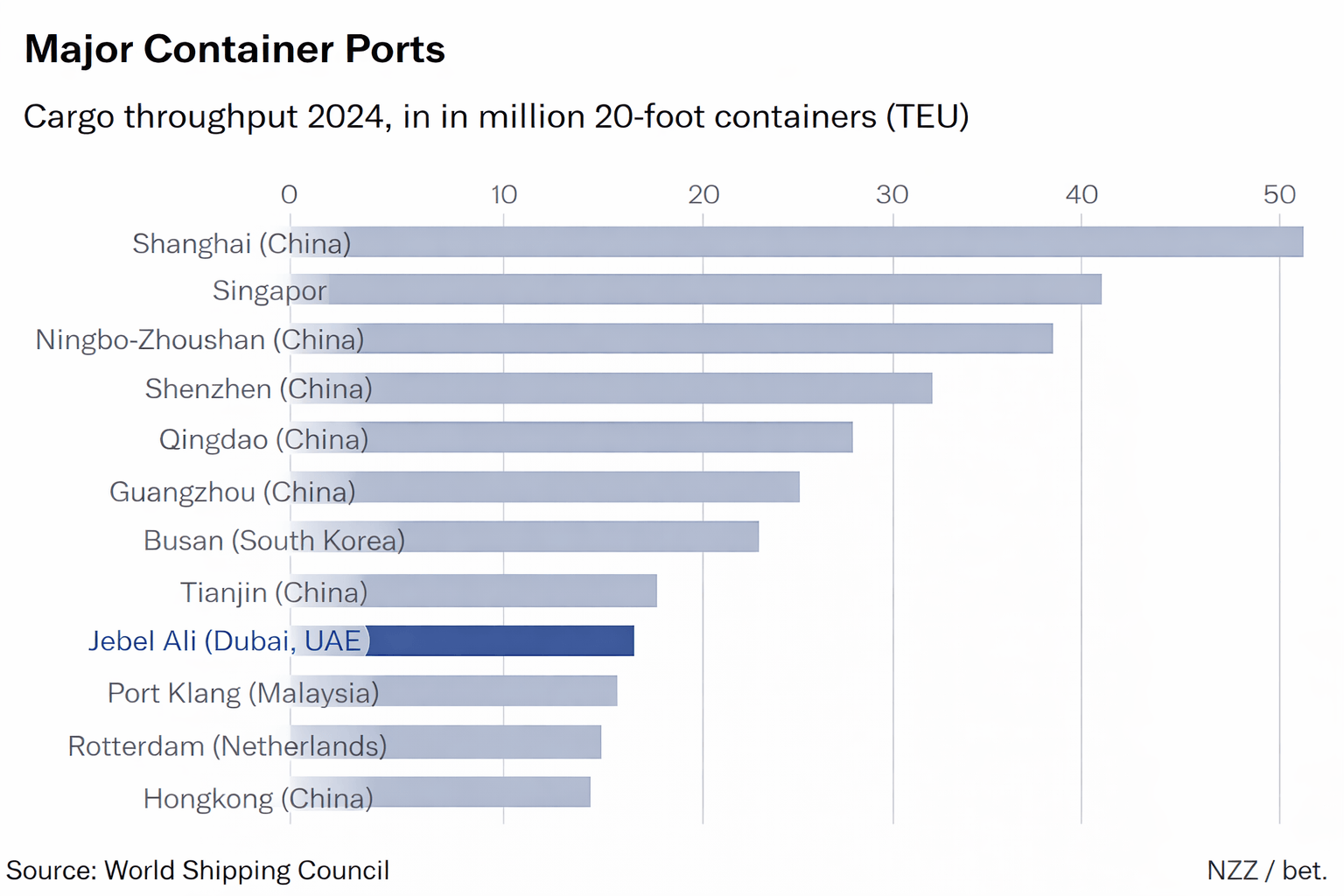

Interestingly, the impact on container shipping routes may remain limited in the short term.

Diagram: Global ranking of the largest container ports measured in TEU, led by Shanghai, Singapore, and Ningbo-Zhoushan.

Most major container shipping routes between Asia and Europe bypass the Persian Gulf entirely.

Only about 2 percent of the global container fleet was located in or near the Gulf region at the start of the crisis.

However, oil and LNG tankers remain highly dependent on Gulf exports, meaning that the Strait of Hormuz continues to represent a major vulnerability for global energy markets.

Worst-Case Scenario: Could the World Face a New Energy Shock?

While most analysts do not currently expect a crisis comparable to the oil shocks of the 1970s, the risk cannot be completely ruled out.

Historical energy crises occurred during:

- the 1973 oil embargo

- the 1979 Iranian revolution

Both events triggered sharp oil price increases, fuel shortages, and global economic disruptions.

Today, the global energy system is more diversified than it was in the 1970s. The United States has become one of the world’s largest oil producers, largely due to the shale oil boom.

Nevertheless, the Gulf region remains a key hub for global energy exports.

Some financial institutions estimate that if the Strait of Hormuz were closed for an extended period, oil prices could rise by as much as $50 per barrel.

Similarly, analysts suggest that a prolonged interruption of LNG exports could push European gas prices to around €74 per megawatt hour, representing a potential increase of more than 130 percent compared with pre-conflict levels.

Why Asia Could Be Hit Hardest

Asian economies rely heavily on imported energy from the Gulf region.

Countries such as:

- China

- Japan

- South Korea

- India

depend on oil and LNG shipments that pass through the Strait of Hormuz.

This creates a double vulnerability:

- higher energy prices

- longer logistics routes and freight costs

Industries with tight margins—such as electronics manufacturing, consumer goods, and industrial components—can quickly lose cost advantages if energy and shipping costs rise significantly.

Why Nearshoring in Mexico Could Benefit

In this environment, the relative competitiveness of nearshoring in Mexico increases for companies serving the North American market.

Several structural advantages explain why.

Shorter Supply Chains

Nearshoring reduces reliance on long maritime routes between Asia and North America.

Production in Mexico allows goods to move by truck or rail, reducing exposure to disruptions on global shipping lanes.

Integration with the North American Energy System

Mexico is closely connected to the United States through pipelines, electricity markets, and trade agreements.

This integration strengthens energy security compared with many Asian manufacturing hubs that depend on imported fuel.

Faster Response Times

Nearshoring enables shorter lead times and greater operational flexibility.

Companies can respond more quickly to demand fluctuations, engineering changes, or supply disruptions.

Stronger USMCA Supply Chains

Production located within North America also benefits from USMCA trade rules, which can provide tariff advantages and regulatory certainty.

What This Means for Companies Expanding to Mexico

For companies evaluating global supply chain strategies, the Strait of Hormuz crisis serves as an important stress test.

Key questions include:

- How sensitive are your production costs to energy price shocks?

- How dependent is your supply chain on long maritime routes from Asia?

- Could nearshoring improve resilience for North American demand?

In many cases, the answer is not to relocate entire supply chains overnight.

Instead, companies increasingly adopt hybrid strategies, combining Asian production with regional manufacturing hubs closer to key markets.

For companies serving the United States and Canada, Mexico is emerging as one of the most attractive locations for such regional production platforms.

FAQ

Why is the Strait of Hormuz so important?

Because a large share of global oil and LNG shipments passes through it, disruptions can quickly affect energy prices, freight costs, and global supply chains.

Could a closure trigger a global energy crisis?

A prolonged closure could cause major price spikes. However, diversified energy production and strategic reserves make a crisis similar to the 1970s less likely.

Which regions are most exposed?

Asian economies are particularly vulnerable because they depend heavily on imported oil and LNG from the Gulf region.

Why could Mexico benefit from this situation?

Nearshoring in Mexico reduces exposure to long maritime supply chains and integrates production into the North American energy and logistics system.