Mexico’s Industrial Real Estate Market in 2025

Why 2025 Is a Decision Year for Industrial Real Estate in Mexico

For CEOs, COOs, and operations leaders, 2025 is not about whether Mexico remains relevant—it is about timing, risk, and execution. Nearshoring, U.S. trade policy, and supply-chain realignment continue to reshape Mexico’s industrial real estate market, creating both opportunity and uncertainty.

Since 2018, tariffs on China have structurally increased demand for industrial real estate in Mexico, especially for warehouses, manufacturing plants, and build-to-suit facilities. While demand remains strong, market conditions in 2025 require sharper decision-making than in previous years.

Nearshoring Continues to Reshape Mexico’s Industrial Real Estate Market

Nearshoring remains the single most important driver of industrial real estate demand in Mexico. Global manufacturers continue shifting production closer to the U.S. to reduce lead times, mitigate geopolitical risk, and stabilize supply chains.

Mexico benefits from:

- proximity to the U.S. market

- USMCA trade access

- competitive labor costs

- established manufacturing ecosystems

However, political developments in the U.S.—including renewed tariff rhetoric and USMCA renegotiation signals—add complexity to industrial real estate decisions in 2025.

China’s Expanding Footprint in Mexico’s Industrial Real Estate

Chinese manufacturers play a growing role in Mexico’s industrial real estate market.

Between Q3 2021 and Q2 2024:

- 27 million sq. ft. of industrial space absorbed

- 9 million sq. ft. annually on average

- Peak leasing of 4.8 million sq. ft. in Q2 2022

Many Chinese companies use Mexico as a manufacturing base to maintain access to the U.S. under USMCA rules of origin. While this supports demand for industrial parks and warehouses in Mexico, it also increases political scrutiny from Washington.

In 2024, Chinese leasing activity slowed, reflecting short-term caution—not a structural exit.

Vacancy Rates and Absorption Across Key Industrial Markets

Mexico’s major industrial markets represent nearly two-thirds of total national inventory.

Top Markets by Gross Absorption (2024)

- Monterrey: 15 million sq. ft.

- Mexico City: 9 million sq. ft.

- Querétaro: 6 million sq. ft.

Markets With Higher Vacancy

- Ciudad Juárez: 10%

- Tijuana: 5.8%

- Reynosa: 5.3%

Rising vacancy in some border markets reflects aggressive speculative development ahead of demand that normalized in 2024—particularly as Chinese leasing slowed from 6.5 million sq. ft. (2023) to 3.7 million sq. ft. (2024).

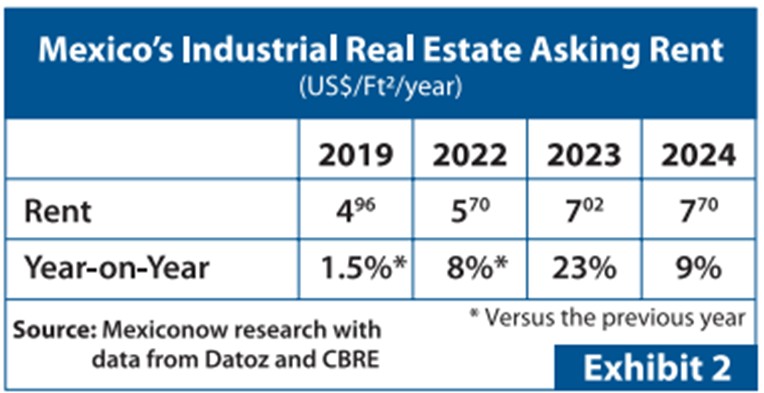

Industrial Rent Trends: Five Years of Structural Growth

Industrial real estate rents in Mexico increased approximately 50% over five years, driven by two structural forces:

1. Nearshoring Demand

Tight supply in Monterrey, Mexico City, Guadalajara, and Tijuana pushed rents upward as available Class A space disappeared.

2. Construction Cost Inflation

Rising steel, concrete, copper, and lumber prices in 2022 permanently reset development costs. While prices stabilized in 2024, rents remain elevated.

Example:A 100,000 sq. ft. Class A distribution facility in Guadalajara reached USD 80–90 per sq. ft. in 2024.(Cushman & Wakefield).

Regional Growth Patterns in Industrial Real Estate

In 2024, Mexico’s total industrial stock expanded 6%, reaching 1.11 billion sq. ft.

Fastest-Growing Regions

- Monterrey: +12.5%

- Guadalajara: +10.5%

- Saltillo: +5.9%

- Tijuana: +5.6%

- Bajío Region: +5.3%

A key market shift occurred with Prologis’ acquisition of Terrafina’s 41 million sq. ft. portfolio, consolidating 8.1% of national market share under one landlord—signaling institutional confidence in Mexico’s industrial real estate fundamentals.

Key Challenges for Industrial Real Estate in 2025

Energy Availability

- Medium-voltage power delays affect industrial timelines

- Thousands of MW in private projects remain stalled

- Energy feasibility now ranks as a top site-selection risk

Security Risks

- Cargo theft increases logistics costs

- Investors assess micro-location security more closely

- Industrial parks with controlled access gain preference

Policy and Trade Uncertainty

- USMCA renegotiation risks

- Potential U.S. tariff pressure

- Increased regulatory scrutiny on foreign manufacturers

These risks do not eliminate demand—but they reward better site selection and execution.

2025 Outlook: What Industrial Investors Should Expect

Despite normalization after the initial nearshoring surge, Mexico remains the strongest industrial real estate market in the Americas.

2025 Expectations

Moderate vacancy increases in oversupplied submarkets

- Rent stabilization in select regions

- Continued strength in Monterrey, Saltillo, Querétaro, Guadalajara, and Mexico City

- Mexico’s role in North American supply chains remains structurally intact.

Conclusion: Opportunity With Higher Execution Requirements

Industrial real estate in Mexico is no longer a simple growth story—it is a selection and timing story.

Companies that:

- evaluate location carefully

- confirm utilities early

- understand regional differences

- align industrial real estate with operational strategy

- will continue to outperform in 2025.

FAQ – Mexico’s Industrial Real Estate Market

Why are industrial rents in Mexico rising?

Due to sustained nearshoring demand, limited Class A supply, and higher construction costs.

Is the slowdown in Chinese leasing permanent?

No. It reflects short-term political caution rather than a structural retreat.

Which markets offer the best industrial real estate opportunities in 2025?

Monterrey, Saltillo, Querétaro, Guadalajara, and Mexico City.

What risks should investors monitor most closely?

Energy availability, security conditions, trade policy, and permitting timelines.

Will nearshoring continue despite political uncertainty?

Yes. Supply-chain resilience and proximity to the U.S. remain strategic priorities.