Mexico Mid-2025 Trade & FDI Outlook: Resilience in a Fragmented Global Economy

Executive Summary

Mexico closed the first half of 2025 with a USD 1.4 billion trade surplus and USD 55.6 billion in FDI inflows, defying global protectionism and tariff volatility.

Exports remain stable, USMCA usage is increasing, and manufacturing-led investment continues to expand. While geopolitical risks persist, Mexico is strengthening its position as North America’s most resilient export platform.

Trade Performance in 1H 2025: Stability Under Pressure

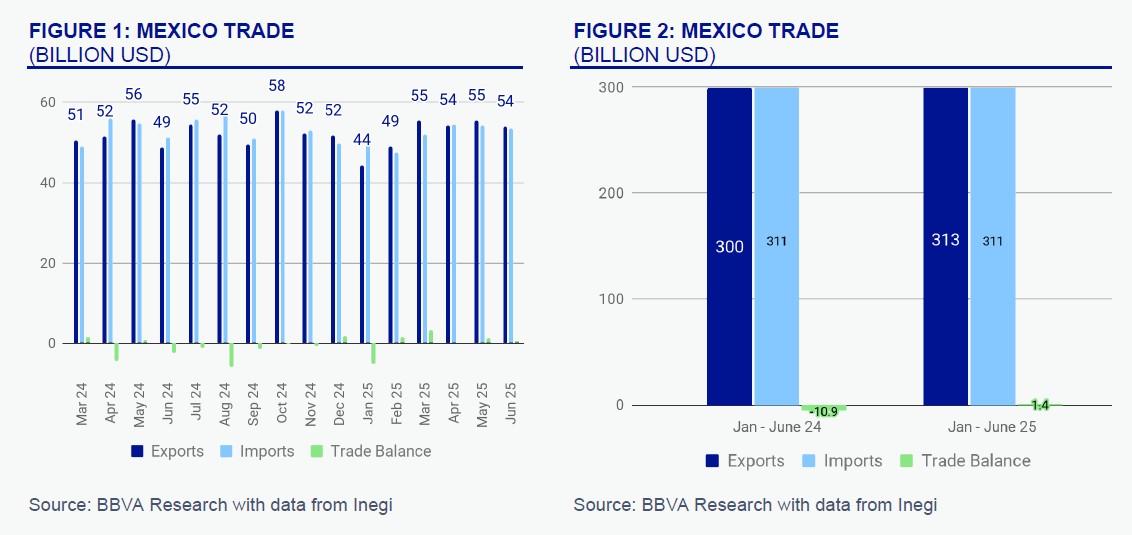

Between January and June 2025:

- Exports: USD 313 billion (+4.3% YoY)

- Imports: USD 311 billion (+0.2% YoY)

- Trade balance: USD +1.4 billion

Monthly export levels remained in a stable band between USD 50–56 billion, signaling structural export strength despite global uncertainty.

Monthly Mexico exports, imports and trade balance from March 2024 to June 2025 showing stable export performance.

The data highlights that Mexico’s export engine is not overheating nor contracting — it is stabilizing.

Manufactured goods account for nearly 90% of exports. Notably, agriculture and livestock have overtaken oil as the second-largest export category — a sign of export diversification.

Trade Structure: U.S. Dominance with Strategic Diversification

The United States absorbed over 83% of Mexican exports in 1H 2025, reinforcing deep North American integration.

However, Mexico’s import structure reveals a complementary pattern:

- China represents 20.1% of total imports

- Mexico increasingly serves as a bridge economy between Asia and the U.S.

This positioning allows Mexico to integrate Chinese intermediate goods while exporting finished goods duty-free to the U.S. under USMCA.

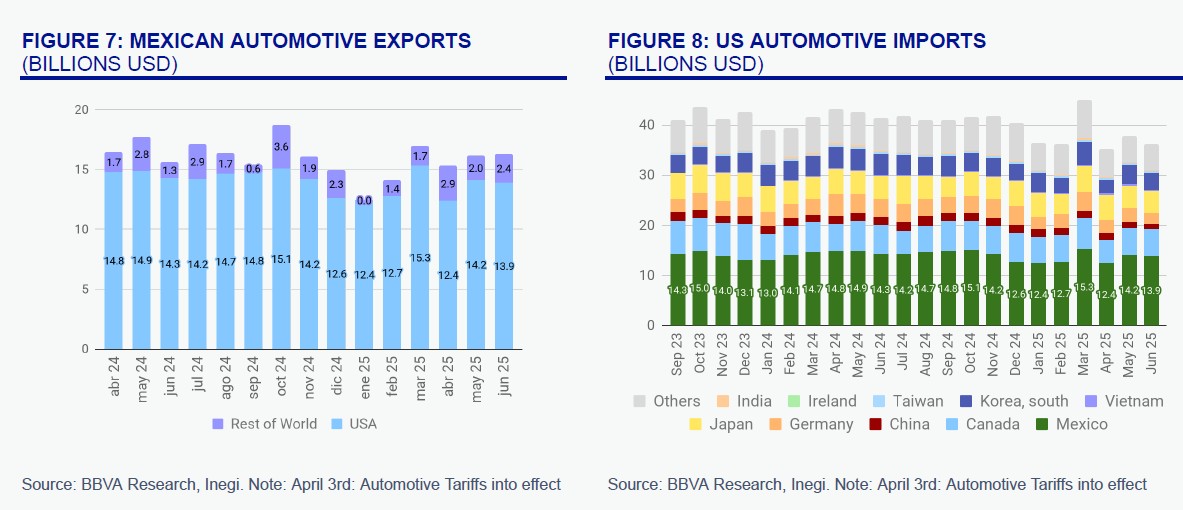

- Mexican automotive exports in billions USD from April 2024 to June 2025.

- US automotive imports by country showing Mexico’s share through mid-2025.

- Mexico trade comparison January to June 2024 versus 2025 showing export growth and trade surplus recovery.

The trade balance improved significantly compared to 2024, underscoring structural competitiveness.

Tariffs & Automotive Performance: Complexity, Not Collapse

The average effective U.S. tariff on Mexican exports stood at 8.28% in June 2025 — considerably lower than many competing markets.

Key elements include:

- 50% duties on steel & aluminum (Section 232)

- 25% automotive tariffs partially offset by U.S. content deductions

- 0% tariffs for compliant USMCA auto parts

- 82% of exports entering duty-free

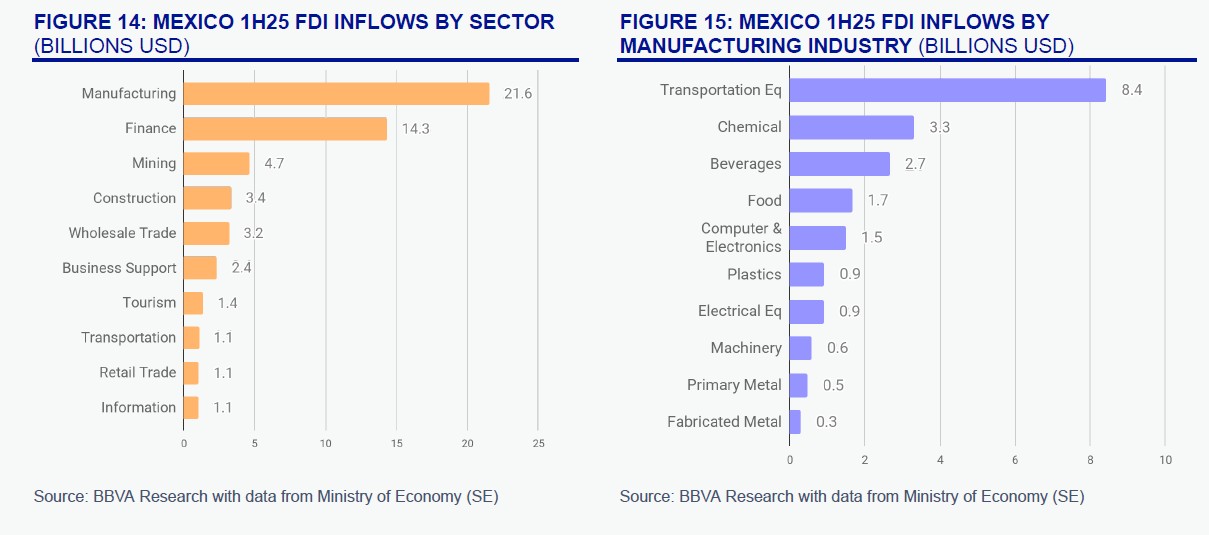

FDI Inflows: Nearshoring Momentum Accelerates

Mexico attracted USD 55.6 billion in FDI in 1H 2025, an 8.2% increase over the prior year.

Manufacturing remains dominant.

- Mexico 1H 2025 FDI inflows by manufacturing industry led by transportation equipment.

Transportation equipment, chemicals, beverages, and electronics dominate — reinforcing Mexico’s industrial depth.

Although automotive exports to the U.S. fell 5.6% YoY, growth toward other markets (+9.6%) helped offset the decline — confirming geographic diversification.

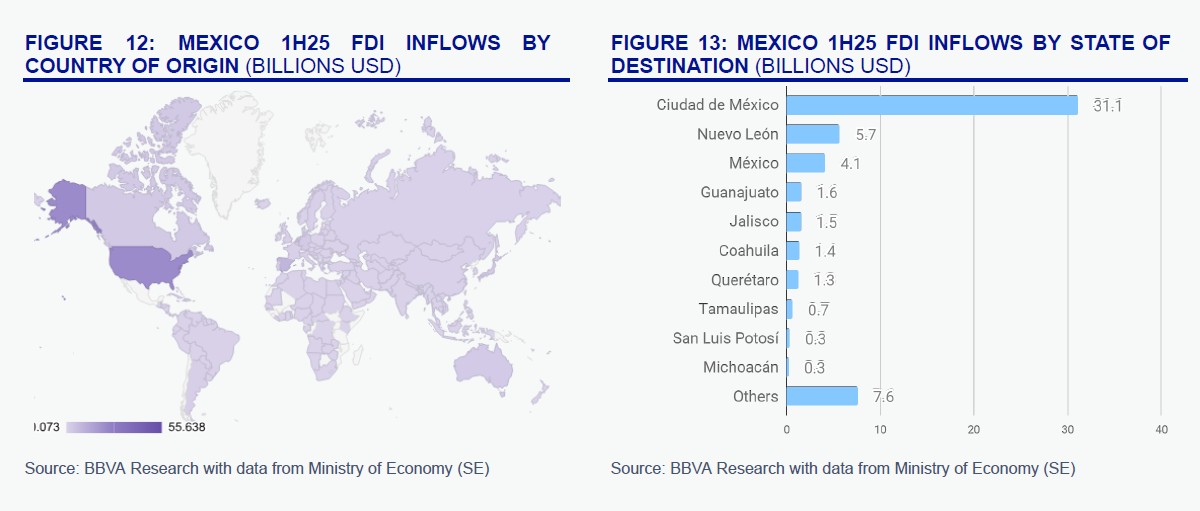

FDI by Country & State

Mexico 1H 2025 FDI inflows by country of origin highlighting United States as the primary investor.

Mexico 1H 2025 FDI inflows by country of origin highlighting United States as the primary investor.

Strategic Implications for Businesses

Mexico’s resilience stems from three pillars:

- USMCA-based trade certainty

- Industrial ecosystem depth

- Policy alignment with nearshoring

If USMCA utilization expands further and tariff clarity improves, Mexico’s effective tariff exposure could drop to near 4%, positioning it as the most competitive export base in the Western Hemisphere.

Policy Support: Infrastructure & Institutional Backing

Key policy initiatives include:

- Nearshoring Decree (tax incentives for EV & semiconductor sectors)

- Polos de Bienestar industrial zones

- IMMEX 4.0 customs modernization

These are not short-term measures — they are structural positioning tools.

Conclusion: From Defensive Resilience to Strategic Advantage

Mexico is no longer merely weathering global volatility.It is capitalizing on fragmentation.

With stable exports, rising FDI, and strong USMCA integration, Mexico is reinforcing its role as the core manufacturing platform for North America.

If tariff friction moderates, Mexico’s competitive gap over Asia could widen further.

FAQ – Mexico Mid-2025 Outlook

Did Mexico maintain a trade surplus in 2025?

Yes, USD 1.4 billion in 1H 2025.

How much FDI did Mexico receive in 1H 2025?

USD 55.6 billion.

Which sector attracts the most FDI?

Manufacturing, especially transportation equipment.

Are U.S. tariffs hurting Mexico?

Some sectors are affected, but most exports still enter duty-free under USMCA.

Is nearshoring still accelerating?

Yes — FDI growth confirms ongoing relocation momentum.