Nearshoring in Mexico: 346 Investment Announcements Signal Structural Momentum

Executive Summary

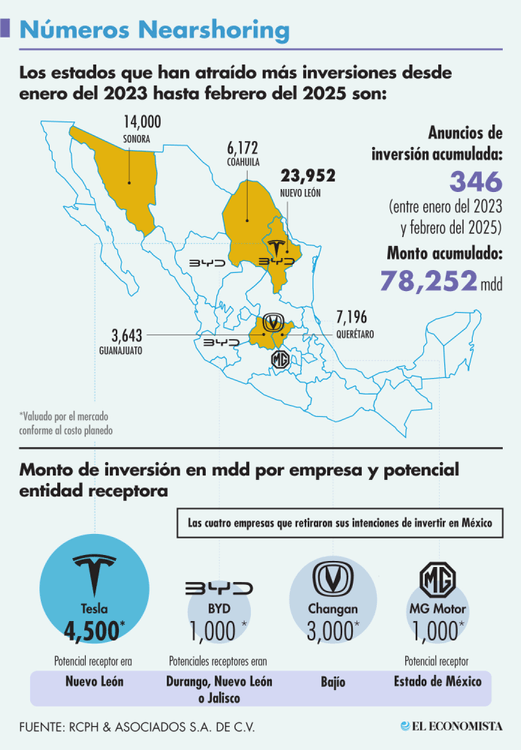

Between January 2023 and February 2025, Mexico recorded 346 investment announcements totaling USD 78.2 billion, reinforcing its position as a primary nearshoring destination in North America.

Although several high-profile mobility projects were withdrawn, the broader trend confirms that nearshoring in Mexico remains structurally intact, with strong activity in automotive, energy, real estate, and advanced manufacturing.

The slowdown in early 2025 reflects political caution — not structural weakness.

Mexico’s Nearshoring Momentum: 346 Projects in Two Years

According to RCPH & Asociados, Mexico attracted 346 investment announcements between January 2023 and February 2025, with a cumulative value of USD 78.2 billion.

This volume underscores continued confidence in Mexico’s:

- geographic proximity to the U.S.

- USMCA trade stability

- established industrial clusters

- supplier ecosystem maturity

However, investment announcements are not identical to capital deployment — and that distinction matters for strategic evaluation.

Map of Mexico showing 346 nearshoring investment announcements between 2023 and 2025 totaling USD 78.2 billion.

Withdrawals: A Reality Check for Nearshoring 2.0

Despite strong figures, approximately USD 10 billion in investment commitments were withdrawn, primarily by mobility and EV-related firms including Tesla, BYD, Changan, and MG Motor.

The main driver was rising U.S.–China trade tension and tariff uncertainty.

This does not signal a collapse of nearshoring in Mexico.It signals that geopolitical filtering is now part of capital allocation decisions.

Investors are prioritizing:

- regulatory predictability

- tariff clarity

- long-term USMCA security

Sectoral Distribution: Manufacturing Remains the Core Driver

The sector breakdown of announced investments confirms that nearshoring in Mexico remains manufacturing-led.

- Automotive: USD 27.4B (35%)

- Energy: USD 19.7B (25%)

- Real Estate: USD 10.5B (13%)

- Technology: USD 5.8B (7%)

Automotive and industrial production remain anchor sectors, reflecting Mexico’s integration into North American supply chains.

Energy’s share also highlights the importance of infrastructure capacity to sustain continued foreign direct investment in Mexico.

February Peak and 2025 Cooling

February 2024 marked the peak with USD 6.27B in announcements.Early 2025, however, recorded only 19 announcements worth USD 3B.

This cooling phase aligns with:

- renewed U.S. protectionist rhetoric

- tariff risk under Trump administration

- investor reassessment of supply chain exposure

The shift is cyclical caution — not structural reversal.

Strategic Projects That Sustain Momentum

Despite withdrawals, major industrial players continue expanding operations, reinforcing the durability of foreign direct investment in Mexico.

Notable examples include:

- Mota Engil (Portugal) – USD 3B fertilizer plant

- Toyota – USD 1.45B manufacturing upgrades

- Citic Dicastal – USD 600M aluminum plants

- Solarever – USD 1B EV battery facility

- Bosch, Siemens, Schneider Electric – capacity expansions

- Makino & NIDEC – Japanese industrial upgrades

These projects demonstrate that nearshoring in Mexico extends beyond EV headlines into diversified industrial sectors.

Nearshoring 2.0: What Comes Next?

The concept of “Nearshoring 2.0” reflects a shift from opportunistic relocation to structured regionalization.

Key drivers for a second wave:

- supply chain resilience over cost arbitrage

- energy transition manufacturing

- EV and battery localization

- semiconductor and industrial automation capacity

Mexico’s challenge is no longer attracting attention.It is converting announcements into executed projects.

Conclusion: Momentum with Measured Caution

Mexico’s 346 investment announcements totaling USD 78.2 billion confirm that nearshoring in Mexico is not a temporary phenomenon.

However, the moderation in early 2025 shows that:

- geopolitical clarity matters

- tariff stability influences capital flow

- institutional predictability determines execution

Nearshoring in Mexico remains structurally sound — but increasingly conditional.

FAQ – Nearshoring and Investment in Mexico

How many investment announcements did Mexico receive between 2023 and 2025?

346 announcements totaling USD 78.2 billion.

Did Tesla cancel its investment in Mexico?

Tesla and several mobility firms withdrew or paused commitments due to tariff and geopolitical uncertainty.

Is nearshoring in Mexico slowing down?

Short-term announcements have cooled, but structural drivers remain intact.

Which sector leads nearshoring investment in Mexico?

The automotive and manufacturing sectors represent 35% of total announcements.

What is Nearshoring 2.0?

A second phase of regionalized production focused on resilience, electrification, and North American integration.