Tariffs Reshape North America’s Auto Industry: Mexico Takes Center Stage

Introduction: A Brave New World for Autos

North America’s automotive industry is entering uncharted territory. With a 25% tariff on imported light vehicles now in place under the Trump administration, supply chains are being forced to adapt in real time. Guido Vildozo, Associate Director for Automotive Consulting at S&P Global Mobility, described this shift as “a brave new world,” emphasizing that the disruption is reshaping how automakers plan production, sourcing, and sales strategies across the continent.

While the tariffs apply broadly to imported vehicles and parts, exceptions exist for cars built in Mexico and Canada that comply with USMCA rules of origin. This carveout has given both countries an edge, even as the wider industry braces for structural changes.

The Immediate Shock: Layoffs and Plant Disruptions

The tariffs, effective April 3, 2025, immediately rattled automakers:

Temporary layoffs were announced at assembly plants in the U.S., Canada, and Mexico.

OEMs revised production schedules to manage higher costs.

Carmakers began holding inventory at borders or delaying launches to assess financial impact.

By May 3, a second round of tariffs on imported auto parts added further complexity. While Mexico- and Canada-made components that meet content thresholds were exempt, parts produced elsewhere faced either a 25% levy (for listed items like engines, transmissions, and suspensions) or a 10% duty for everything else.

This patchwork of rules created confusion but also highlighted Mexico’s strategic position: according to the National Auto Parts Industry Association (INA), 92% of Mexican components already comply with USMCA standards, making the country a relatively safe harbor amid tariff turmoil.

Mexico’s Auto Industry: Record Production, Shifting Exports

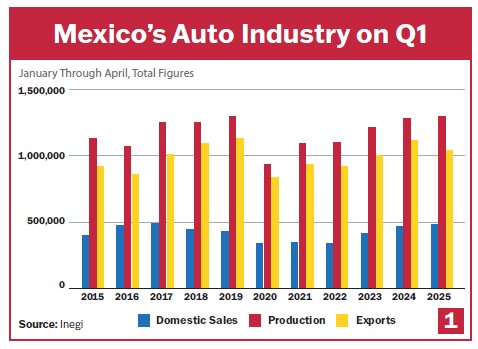

Despite turbulence, Mexico’s auto industry continued to post impressive figures in Q1 2025.

Production Trends

In March 2025, Mexico produced 338,669 light vehicles, up 12.1% year-over-year.

Q1 output reached 973,485 units, the second-highest first-quarter volume on record (+4.8% vs. 2024).

By the end of April, total production hit 1,299,554 vehicles, a modest 0.9% increase compared to the same period in 2024.

Exports Under Pressure

Exports dropped 7.3% year-over-year, totaling 1,032,819 units through April.

This decline reflects the immediate shock of tariffs and holiday-related downtime at plants.

Domestic Sales Resilience

Mexican domestic auto sales showed surprising strength, climbing 1.4% in Jan–Apr 2025 to 473,323 units, the second-highest level ever recorded for this period.

April sales slipped 4.6%, partly due to Easter holidays, but overall consumer demand remained steady.

📊 [Exhibit 1: Mexico’s Auto Industry, Q1 2015–2025] shows the resilience of production and domestic sales despite tariff-induced export volatility.

U.S. Market Reaction: Consumers Rush to Buy

In the U.S., consumers moved quickly to secure vehicles before tariff-driven price hikes hit dealer lots.

March 2025 sales: 1.61 million light vehicles (+11% YoY).

April 2025 sales: 1.49 million vehicles.

The 12-month rolling average (SAAR) stood at 17.6 million units.

Brands like Toyota, Kia, Mazda, and Ford posted strong gains, while Infiniti, Jeep, and Audi struggled. Mexico-made vehicles, in particular, experienced a notable surge in U.S. demand.

📊 [Exhibit 2: U.S. Sales of Mexico-made Vehicles, Q1 2024 vs. Q1 2025] highlights winners and losers:

Biggest gainers:

Nissan Versa (+156%)

Nissan Sentra (+36%)

Chevy Equinox (+31%)

Mustang Mach-E (+21%)

Decliners:

Chevy Blazer (-12.6%)

Mazda CX-30 (-26%)

GMC Terrain (-27%)

This short-term rush, however, is expected to fade as pre-tariff inventory runs out and dealerships adjust pricing strategies.

Automaker Strategies: Discounts, Rebates, and Delays

To soften the blow of tariffs, the U.S. government announced relief measures:

Duty-free policy for USMCA-compliant parts (temporary).

Tariff rebates up to 15% of vehicle value for 2025, dropping to 10% in 2026 before expiring.

Measures to avoid stacked tariffs on overlapping items.

Still, automakers are experimenting with different approaches:

Some are offering discounts and price assurance programs.

Others are halting production or delaying shipments until costs are clearer.

Leasing strategies are gaining ground, especially for premium brands where up to 60% of vehicles are leased.

According to Erin Keating of Cox Automotive, “April and May may be strong for sales, but production disruptions will likely hit this summer.”

Mexico’s Strategic Edge Under USMCA

One reason Mexico is weathering the storm better than other export hubs is compliance. Nearly all major assembly and component plants already meet USMCA rules, allowing them to avoid the steepest tariffs.

Looking ahead:

Vehicles and parts from Mexico and Canada face a 25% tariff through 2025, but only on non-U.S. content.

In 2026, that rate is expected to drop to 12%, offering relief to regional players.

For non-North American imports, the full 25% rate stays through 2026, before possibly falling to 15% in 2027.

This differential treatment could accelerate nearshoring of supply chains to Mexico, reinforcing its role as a production hub for affordable compact SUVs and sedans that dominate U.S. demand.

The Road Ahead: Uncertainty and Opportunity

The auto industry is clearly entering “uncharted territory.” Analysts agree that tariffs will:

Create short-term demand spikes in the U.S. as buyers rush to avoid higher prices.

Lead to production slowdowns later in 2025 as inventories adjust.

Push OEMs to rethink their supply chains, especially for compact vehicles, many of which are imported today.

As Guido Vildozo of S&P Global Mobility observed, half of U.S. customers are looking for cars priced below $37,000 — a segment dominated by imports. Mexico’s ability to produce these vehicles efficiently makes it central to any solution.

Still, profitability challenges remain. Automakers must weigh whether moving production into the U.S. is feasible for compact models, or whether leasing and other financing innovations will bridge the affordability gap.

Conclusion: Mexico at the Heart of a Shifting Industry

The 2025 tariff shock is reshaping North America’s auto sector, but Mexico is proving resilient. With record-high production levels, strong domestic sales, and rising U.S. demand for Mexico-made vehicles, the country stands to gain even as global supply chains adjust.

If the expected tariff reductions materialize by 2026–2027, Mexico’s competitive edge under USMCA could strengthen further, making it not only the backbone of North American auto exports but also a leader in affordable vehicle production.

The road ahead may be rough, but Mexico is firmly in the driver’s seat of North America’s automotive transformation.